Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Key Capitol Hill Hearings CSPAN November 19, 2013 2:00am-4:01am EST

2:00 am

of first lady's drug history. it is available for the discounted price of $12 95 cents plus shipping at c- span.org/products. our website has more about the first ladies, including the special section, welcome to the white house, produced by her partner, the white house historical association, which chronicles life in the executive mansion ring the >> there are some serious scholars and women's studies, most departments include their fair share of non-ideological academics who offer straightforward courses, sometimes wonderful courses in the men's, women in literature. ,ut ideologically fervent statistically challenged hard- liners set the tone in most women's studies departments. if there is a department that defies the stereotype emma i would love to visit them. , moderateve women

2:01 am

women, libertarian women, traditionally religious woman, left out. feminismr critique of have led critics to label her as anti-feminist. sunday, december 1, your questions for christina hoff sommers. levin.n mark span2.v on c- john kerry spoke about climate change. remarks for to the organization of american states meeting. >> more than two decades ago i visited rozelle as part of the u.s. legation to the rio summit. this was the first time the global community came together

2:02 am

united to try to address climate change. it was also the trip where i got to know an amazing portuguese speaking woman who three years later would become my wife so i like to. it is a good place. about and i still talk our 12-year-old girl from vancouver. who took the stage at that itmit in order to as she put , "fight for her future." rememberlater i still what she said about climate change. as follows. i am only a child, she told us. yet i know we are in this together and should act as one single world toward one single goal. that aerstood something lot of folks today need to grasp, something still missing from our political debate. i said asaying goes,

2:03 am

moment ago. we need that more than ever now. with respect to this challenge of climate change. decades later we have a lot to learn from that young woman. the newicas have become center of our global energy map. our hemisphere supplies now one fourth of the world's crude oil and nearly one fourth of its coal. we support over one third of global electricity and what that means is that we have the ability and the great responsibility to influence the way the entire world is powered. it will require each of our nations to make some very fundamental policy choices. we need to embrace the energy future over the energy of the , it create i am well aware

2:04 am

have been through these battles in the united states senate. i know how tough it is. i know how many different industries and how many powerful interests there are to push back. have a people, all of us responsibility to bush back against them. climate change is real. is happening. if we do not take significant action as partners, it will continue to threaten not only our environment and communities but as our friends in the caribbean and other island nations now, it will threaten potentially our entire way of life, certainly bears. the challenge of climate change will cost us far more. for its negative impact, and the investment we need to make today in order to meet the challenge. every economic model shows that ended we shy away. our economies have yet to factor

2:05 am

in the monetary costs of doing nothing or doing too little. effects thatng drugs can have on farmers' harvests. andr every hurricane tropical storm that leaves a trail of destruction in their wake. notcost of fires that did earn us versus lee and frequently as they do today because of the increased dryness. the increasing signs of less of water for the himalayas as the glaciers shrink and therefore as the great rivers of china and other countries on one side and india on the other are threatened, as billions of people see their food and food security affected among these are real challenges and they are not somewhere in the future. we are seeing them now. for all these reasons, combating

2:06 am

climate change is an urgent president obama and myself and we know that we are one of the largest contributors to the problem. there are 20 nations that contribute over 90% of the problem. that is why president obama unveiled the new climate action plan to drive more aggressive to mystic policy on climate change than ever before and the good news is the agenda he has put together is one specifically designed to be done by administrative order so you do not have to wait for congress to act. >> coming up, the conversation with lyrical house reporter cal cheney. and a look at health care price caps. streamline theo way the pentagon does business. the senate foreign relations had the response to

2:07 am

the typhoon that hit earlier this month. officials will testify tomorrow morning live it 10:30 a.m. eastern on c-span three. law enforcement and regulatory officials will take questions about digital currencies such as the bitcoin. live coverage at 330 a.m. eastern also on c-span3. >> every weekend since 1998, book tv has brought you the top nonfiction authors including hannah rosen. quick thinking recently women's identity as they are tied to their work in a way that we may not like, in a way we might found -- find disturbing and unnatural but is true. when i look at someone like mark waselissa mayer, when she visibly pregnant and asked how

2:08 am

much maternity leave do you want to take and she said basically none will like the fact that such women exist, it is not the way i would do that. i took plenty of maternity leave. i feel like that is a growing number, the kind of woman that there can be space for and the fact that there are some stay- at-home dads who are very happy and who do not live in portland, oregon, that is ok, too. >> we are the only national television network devoted to nonfiction books and throughout the fall we marking 15 years of book tv on c-span2. c-span. we ring public offense from washington directly to you, putting you in the room i congressional hearings, white house events, briefings, and conferences and offering complete gavel-to-gavel coverage of the u.s. house all as a public service of private industry. we are c-span. created by the able tv industry

2:09 am

34 years ago and funded by your local cable or satellite provider. you can watch us in hd. >> a reporter talks about the problems with the governments health care website i congressional oversight of the new health care law. from washington journal, this is one hour and 20 minutes. guest is carl "politico." why don't we start with the house vote on friday to remind us exactly what the house is voting on. how is it different? >> the house voted friday pretty .trongly for a bill not a fan of the affordable care act. this was the keep your health plan act or something along those lines. it was intended to get at the issue of people whose plans are

2:10 am

getting canceled. differs is his plan according to supporters of the affordable care act would undermine the law by allowing people to sign up nearly for some of the plans that do not meet the requirements of the affordable care act. it is a plan of getting phased out because of the lack of benefits require the upton bill not only to keep those plans but to sign up for those plans newly in 2014. the president's was different in the sense that he does not want people to remain on those plans long term. period.iving a grace >> one of the critiques in recent years as they were meeting with this one. how important was that? aboutt was significant sided withdemocrats

2:11 am

republicans. the attraction to democrats who are up for reelection all next year. and so while the proposal does not necessarily pass in its current form it shows where the mindset is and where the politics are and there's a lot of concern out there that democrats are vulnerable on this issue of people losing their health plan. >> nancy pelosi, the minority leader stepped in on one of the sunday morning shows to talk about democrats and that vote in health care. here's a look. >> i do not think you can tell what happened next year but i will tell you this. in supporttand tall of affordable care act. we have great candidates who are running for concerned about our economy and concern that government was shut down because of a whim on the part of [inaudible]

2:12 am

they are concerned that overwhelming the american people supports background checks and supports ending discrimination against people in the workplace. all of of these kinds of things. jobs will be the major issue in the campaign as they always are. this is an issue that has to be dealt with. it does not mean it is a political issue so we will run away from it. it is too valuable for the american people. what is important about it is the american people are well served, not who gets reelected. >> any follow-up? clearly wants to turn the page on the crisis of the moment with the affordable care act and the democrats want to do that and the question is will they bill -- will they be able to? there is hope this immediate crisis will pass and they will be able to -- the affordable

2:13 am

care act and all the website albums that have plagued it and these cancellation notices will become a blip on the screen and people will start realizing and recognizing the benefits. we will talk about those other issues next year. we do have kyle cheney to help with any information about the law. the rollout of course, what is happening. we have been talking about the congressional bill and we will get to your calls in just a moment. we want to follow-up on this house bill. aboutw the president is to veto that legislation. is there anything like it in the

2:14 am

works in the senate? >> there is and it is a democratic sponsored bill. the senator has her own proposal which does not go as far as the upton bill. it has somewhat the same effect compared to the upton bill that was a rebuke to the affordable care act. it chastises the president, if you -- for his if you like your health when you can keep it. enabling people to stand plans that do not meet the requirements. the political fate of that bill is an open question. it is not the upton bill. democratsas scary to as the upton bill may have been. it is a sign that democrats are uneasy about the politics of people losing their health plan. >> is there any big hearing or big meetings we should know about? >> i am not 100% sure from the

2:15 am

docket. -- thethat that bill senate will consider that. some form or another. the president tried to take that off the agenda with his own fix but it does not seem to have mollified everyone. i think -- we have not heard the last of the landrieu bill. caller: thank you for c-span. i had my policy canceled. i am a senior citizen. i lost my mate november 8 and he was 16 years older than i am. i am going to be 82. he got canceled because of pre- existing diseases, but he went which i cannot

2:16 am

praise. hold bunch off of my shoulders. after listening to the president and i had gotten a policy that was a much better than what they , those referrals, it took three weeks to get a referral. i that time the cancer had grown twice the size so i called the insurance company and told them i had listened to the president and if they -- if this went through, would they reinstate me even though i had another policy. this is their answer. not cancel you because of the affordable care act. we were already in the process of selling to another insurance agency. they changed their story completely and that is what

2:17 am

these people are going to find out. it is not the affordable care act, it is insurance companies. guest: i was wondering if betty lou was on medicare. anyone over 65 is not meant to be entering the insurance programs for obamacare. but she did have a point that insurance companies in a lot of cases are the ones that are changing these plans. one thing that the white house is try to emphasize is that even prior to the affordable care act insurance companies were the ones making the also changes to people. a lot of these cancellations or not necessarily directly derived from his health law. i think that is the point, he's really try to hammer it home. host: here's your updated piece in "politico." from today. states divided over complying with obamacare fix. regulators are dressing to

2:18 am

president obama's rescue after an attempt to fix a rising wave of canceled policies. tell us more. guest: when president obama announces fixed last week, he kicked the problem . insurance -- to insurance companies and state insurance regulators. what we have seen is state regulators, even if they want to comply with the president's wishes, they might be constrained because they have to do it quickly. they only have a few weeks to really get their rules and regulations updated. especially when the law changes, they may take months or more. a lot of them are saying, even if we were interested we couldn't do it great a lot of them are saying flat-out they're not interested because they don't want to reintroduce these substandard plants back into the market. it remains to be seen how many people the president's fix will

2:19 am

apply to. if states don't go along it could be a small number. host: let's hear from a shell in minneapolis. republican for kyle cheney. six months ago one of your ladies from the kaiser institute mentioned and something that no one is really talking about recently is the fact that these people, they keep talking about subsidies for people who might need them. apparently it is in the law that if your state did not expand medicaid people in your state do not qualify for the subsidy. they did not have enough money to qualify everybody. that is going to hit the fan. paul ryan, every time he gets in -- at these congressional hearings, he mentions if he is talking to these representatives

2:20 am

for the health care plan, he mentions to them, by the way, there is a callback feature and if they accidentally give someone a subsidy that is not supposed to get a subsidy, technically, they are supposed to go back after the next year when that is fleshed out with the tax system. they are supposed to go back and call this money back. saidall these congressmen you think of subsidy, they do not understand. people cannot even afford with a subsidy. what is really different about this, people are not used to paying a monthly payment for their health care. , they dothese people not realize that people out there cannot afford these plans. you get someone who is paying $200 a month but that is $2400 a year and you find out there is a $6,000 deductible.

2:21 am

before the insurance companies have to pay anything. >> on medicaid expansion i am not sure if there is a availableip that are through the exchanges. you're right that states that have not expanded medicaid, it is not that they cannot give out subsidies. it is that they lose out on billions and billions of dollars that would go to helping cover the medicaid population which is the lowest income people in the state. states that turn that down, their existing medicaid programs no matter how ungenerous they are and narrow there for people or they do not cover single adults or a child with adults, those would remain in place for the most part in states that are not accepting medicaid dollars. on the other point, you said people who get a subsidy that they were not entitled to would have that clawback and that is true.

2:22 am

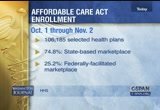

the process called reconciliation, at the end of the first year when people go to file their taxes, they will say how is your income, was it what you expected it to be and if your income was higher than you thought you have to give back a portion of your tax credit. >> a little bit about where we have been and where we are headed on the affordable care act. begin a would be set to little more than a year. a few months, i should say. january 1, 2014. consumers can wait until march 31 of next year to save -- signout -- sign up without a penalty. 106,000 plus elected health plans are out there. 74.8 our state market based lans and the rest, 25.2%, federally phyllis said -- facilitated plans. a couple of other figures here to let you know about. under one million have gone

2:23 am

through the process but have not picked a plan. under 400,000 are eligible for medicaid or the children's health insurance program. of course the numbers who have signed up have been very much in the news lately. saying the government lately and what will they report again? >> we will expect those on a monthly basis. guest: on a monthly basis, early to mid december. i will be a lot more significant. it will show progress they have made fixing the website, which has really blocked people. we will get a sense of the progress they are making. we're going to find out if young people are signing up. what is not in those numbers is the mix of people that are getting covered. the obama administration needs young people to sign-up to help offset the cost of the older and sicker population. we're supposed to get a clearer breakdown of that in december. those numbers will matter more than the first round, which sent the baseline going forward.

2:24 am

whenever you described, that 945,000 that have gone through the process but have not selected a plan, that is buoying the white house. all people have to do is click on a health plan. what they are hoping is that people are actually shopping, comparing plans and taking their time, they are not stuck at a blue screen error message. they are hopeful that those people are in the marketplace. host: 975,407 according to hhs. november 1, that is the date that the administration -- guest: november 30. host: a lot of dates. and numbers out there. november 30, that is the next key date, explain what you are looking for to happen.

2:25 am

we have already seen come over the weekend, expectations being lowered. guest: it has been a steady process of lowering expectation for what november 30 is going to mean. the enrollment system on healthcare.gov, where most states are going to sign up for the new subsidized tax credit waste insurance plans on the exchanges, it has not worked well. it has barely worked but it has slowly gotten better. the white house has called in a team of tech experts to fix the site. they said by november 30, we will have the enrollment system up and running for the vast majority of users. that has been the amorphous part we are trying to pin down. we have seen reports suggesting that that is 80% of people trying to sign up. it is going to be hard for us to pinpoint on the outside whether they actually achieve that. that is the magic they are working with. host: as we go back to calls, one tweet.

2:26 am

"congress is using the aca as an excuse to do nothing." baltimore, you are on with kyle cheney. caller: thank you for c-span. i was curious about something, you did touch on this somewhat. considering the fact that aca was enacted three years ago, not last month, three years ago. obviously, there has been some transitioning in 2010, 2011, 2012. transitioning people out of the bad plans into other plans. has there been analysis on how many people were rotated into new plans during that period, and what the real numbers are with respect to cancellations? whether these were cancellations that happened last month or an accumulation of policies that have been canceled over a period of 3 years.

2:27 am

guest: you are right that there have been studies done, some figures show that this churn in the individual market, where people are losing their plans, they have been losing their plans for a long time. their benefits have been changing. these plans change constantly. they are always transitioning people. what is different about the recent wave is that a lot of the cancellation letters specifically cite the affordable care act. you could argue that that is insurance companies using the cover of the health law to do what they have always been doing, moving people off their old plans and onto new ones. in some sense, it is the result of the affordable care act implementing more stringent and comprehensive benefits. that has resulted in some of the changes going on. host: phil from florida. independent. good morning.

2:28 am

caller: i was recently hospitalized for three days, i was charged tens of thousands of dollars for services that should have cost a minute fraction. of that amount. i think the primary problem with health care is obviously the cost of services. obamacare does not address that. the insurance policies that are available are very expensive. my question is, how many people do you think will actually sign up for these policies? do you agree that the problem with health care is the cost of services? thank you. guest: from a consumer perspective, cost is king. everybody wants to know are they going to pay more in premiums? what will happen with personal health care costs. the affordable care act has mechanisms that limit out-of- pocket expenses. if your insured, you should not pay more than about $6,350 in out-of-pocket expenses a year, that is with a bare minimum plan.

2:29 am

the law does take to on some degree the share of costs that fall on people. the number of people who sign up, the white house is hoping that about 7 million in role in the new exchanges in his first year. that is the goal of the cbo and what actuaries think needs to happen. in order to make the costs work. host: retailers are wary of the health law, they are afraid of losing business. walmart and true value, two of the big companies pointed out here, saying the aca will take a chunk out of consumers' pocketbooks. they might be spending less and stores. there is a tweet here. how are the sign-ups going in states that started their own exchanges? guest: there is a clear

2:30 am

division. when they released numbers, the states that elected to run their own exchanges, by far enrolled more. 14 states, maybe a couple do not report fully, they all had far more sign-ups. even if those did not meet their targets, the division was clear. states running on healthcare.gov had a fraction of the moment. host: three governors write in "the washington post." washington, kentucky, connecticut -- how we got obamacare to work. they have an op-ed in the washington post about their efforts in their states and how things have been going. they make a point that the aca has been successful there. in our states, political and community leaders grasp the importance of expanding health care coverage and have avoided

2:31 am

the temptation to use health- care coverage as political. guest: it is hard to say that there weren't politics and play here too. but for the most part, they are right. governor beshear in kentucky have the ability to establish an exchange and expand medicaid, he could bypass a legislature. because he could implement that without the resistance of the legislature, they were able to see with the law looks like without the political wall or trip wire at every turn. kentucky is an example that everyone points to, this is a state where it is working it was designed. host: kyle cheney is health policy reporter for politico. he is with us, taking your questions and comments about all things health care.

2:32 am

the policy, the rollout, the politics as we have been talking about. one of the voices out there this weekend was senator john barrasso of wyoming. he was on one of the morning shows yesterday to talk about health care. [video clip] >> it is time to start over. this health-care law is terribly flawed. it is broken. it has failed the american people. they are losing insurance, losing their doctor, their premiums are going up. there is going to be a massive taxpayer bailout needed just to deal with the impact of this health-care law. this is not with the american people want. the president did not need to destroy a good health care system to try to make a better one for my that is what we have now. host: one of the gop voices out there. guest: senator barrasso is a doctor, he tends to come from the perspective of someone who has lived in the health system. i think he would be hard-pressed

2:33 am

to find people to agree that today's health care system is good. his argument is that the system under obamacare would be far worse. he is talking about starting from scratch, an idea that republicans continue to speak very calmly about. is increasingly difficult, the longer the affordable care act is implemented and the more people that sign up. even though the numbers we talked about on the low side, it is still about 500,000 people who now health care or are in line for health care in january who did not before. talking about starting from scratch and ripping obamacare off the books is a taller order. host: speak more about that. in "the weekly standard," they asked the question what will republicans offer to replace obamacare? that word "replace," what might happen? this anything significant come?

2:34 am

guest: this has been the republicans' problems is the affordable care act passed, articulating what a replacement would look like. we hear ideas like allowing states to sell across state lines. they use the catchphrase "patient centered care" a lot. the few other ideas floating around in republican circles that do not have the sweeping nature of the affordable care act. maybe that is by design. also, the affordable care act does rely on republican ideas that were brought together in a way republicans can no longer support quickly. a lot of those ideas were from the republican will chest, making it hard to articulate the alternative. host: here is a tweet. "will the dems who voted for the upton bill has a primary challenge so we can vote them out."

2:35 am

guest: they were reacting to their district. it is a great question, whether they will draw -- there will be a more robust debate on the democratic side about the future of health care. one of the things we have heard, if the affordable care act falls apart or if democrats run away from the affordable care act, one of the places they will turn is to single-payer. the idea does not have a lot of political support the states. it is something a lot of people on the left would like. if the affordable care act continues to languish, you may start hearing those voices on the left. whether they challenge people in the primaries or not, i don't know. you may hear that argument raised a little more. host: pennsylvania, lauren is on the line for republicans. welcome. caller: thank you for c-span. i appreciate it. i am commenting on nancy

2:36 am

pelosi's statements. and barack obama's statements. you can keep your health care plan if you would like to. those of us in the republican party and the tea party are warned about this when we spoke about how people were going to lose their insurance. it is a very simple concept, when you have more mandates to provide free services, they are going to increase the rates. just like any company what, they cannot afford to pay for that. taxpayer money supporting like the government does. it was a complete lie. at the president not said that, he would not have won the election. that is the simple fact in regards to why he said what he did. he had to say it or he would not have been reelected. after the election, this whole

2:37 am

year before all this happened, all we heard about was how it was a mandate. the people elected him were in favor of the health-care bill. they were in favor of the bill because they were told that they could keep their current insurance policy. they were not bad policies, it did cover what they wanted. it did not cover new mandates by the health care bill, mental health, men paying for maternity care, women paying for prostate cancer. for them to say that the health- care -- that barack obama's reelection was showing favor of the health-care bill. sure it was, now it is not. guest: you raise some interesting points. one of the things that people sometimes forget is that the president and insurance companies were pretty much allies in getting this bill done. you mentioned the mandates, a

2:38 am

good point. on the flipside, there is the big mandate, the individual mandate. that requires most people to purchase insurance or face a penalty. that is one of the most reviled revisions of the law. that was a provision fair by insurance companies, it would put more people in their plans. including younger and healthier people who do not cost as much to cover. you're are right about new mandates that cost more and can add cost, but by adding millions of new people into the plans -- into these private plans, the hope was that they would balance out that cost and make the law work financially. host: fred, texas, democrat. good morning. caller: good morning. i want to remind everyone what has actually occurred in the years since president obama took office. you will recall that there was a

2:39 am

meeting on the night he became president of gop leaders. they promised one another that they would not vote for anything that he was supporting. they have followed through on that in the years between. recall that the gop members of congress had the opportunity and did participate in planning for the act. and then they just quit. and would not vote for it. the main thing that i want to say is that the gop members of congress are in direct opposition to the terms of the

2:40 am

constitution of the united states. the constitution specifically states the responsibilities of congress, both of the house of representatives and the senate. host: let's hear from -- guest: what that alludes to is how difficulty politics have been. one of the things that have been used as a bludgeon, not a single republican voted for the iteration of the affordable care act that passed into law. because of that, it has been easy for republicans to look back and say this was a democratic bill that passed purely along democratic lines. this was not some great bipartisan entitlement. this was purely ran through by a democratic congress. that has made it difficult to gain traction around the country.

2:41 am

it has been easy for republicans to fight it. the republican points to massachusetts, but that law had huge bipartisan support in the state legislature, making it easy to go back and fix things when they did not work and tinker with it. host: here is a little bit from the president late last week. [video clip] >> those who got cancellation notices do deserve and have received an apology from me. they want, whether we can make sure that they are in a better place and that we meet that commitment. by the way, it is important to note that a whole bunch of folks in congress and others who made this statement, they were entirely sincere about it. the fact that you have got this percentage of people who have

2:42 am

had this impact, i want them to know that their senator or congressman, they were making representations based on what i told them and what the white house and the administrative staff told them. it is on us. it is something that we intend to fix. host: kyle cheney? guest: the president has been getting an earful from congress, democrats in congress, about the fact that they stuck their necks out for him when he said if you like your health plan, you can keep it. democrats parroted him and believed him, believed what he was saying was correct. that made it politically salable to their constituents. now he is out there covering for them. saying if they said that based on what i said, it is on me. i was not -- i did not asterisk that with the fact that some people would lose plans.

2:43 am

host: kyle, new hampshire, independent caller. caller: hi. my problem with the whole thing, maybe it should have been called the deplorable care act. it does not address all of the other medical insurance is that we have. we have insurance is on our workmen's compensation, on our houses come our business, our cities, our states. all of them have medical coverage. why do we need that? why not one, single-payer, then we just take and eliminate all the other insurances? there is more than enough money. why have medical costs gone from 5% when i was a young man to 16%. guest: the cost of entitlements, and the fact that health care consumes 1/5 of the u.s. economy. that is something that both

2:44 am

sides address. the debate has been how do you address that, reforms to medicare and social security, now the affordable care act. the partisan divide has prevented the wholesale look at how to attack those. as for single-payer, i alluded to this earlier, there has not been a whole lot of political constituency pushing for single- payer because it has been a nonstarter politically. particularly in the center and on the right. whether that gains traction is an open question. host: there is a tweet here, i wish the caller was on the phone. what percentage of health care spending is spent in emergency rooms? guest: that is a good question. it is a part of a goal of the affordable care act, get people

2:45 am

out of the emergency rooms. as a place where people go to get their primary care, if they get a cold or a minor injury that you could call your doctor. they go to the emergency room, way more expensive than if you had insurance and saw your doctor on a regular basis, prevented illnesses. the idea is to get that percentage down. that is a cost driver in health, emergency care. host: what do you make of what bill clinton had to say last week just before a president can out and made the change? guest: that put the white house in an uncomfortable position. this is right at the time of the upton bill being talked about and scheduled to vote about it on friday. before that though, president clinton came out and said president obama has got to make good on his progress that if you

2:46 am

like you're playing you can keep it, even if that means a change in the law. since then, president obama endorsed the fixed that did not involve a change in the law. president clinton stepped out a little bit in front of president obama and put them in an uncomfortable position. obama stops short of addressing the upton bill, he has issued a veto threat. clinton forced the white house's hand. is that to help hillary if she decides to run? we are still three years away from 2016, tough to say and evaluate the politics of that. it did force the white house to take a stand, which happened not to be the standard bill clinton identified. host: prior to the upton bill last friday, with the president can on asked for was being described as an administrative mix. how does it work? is assigned by administrative order, is there legislative action? guest: although they have issued is a letter that they sent to state insurance commissioners

2:47 am

from cms, one of the agencies implement the law. it says, just so you know we will not enforce the minimum standard provisions for plans in the individual market for people who currently have them. if those are going to be canceled, we will look the other way and say you can continue to implement those. you touched on the legal basis. hearing a lot of people who say there is not a legal basis. the law has certain requirements, they are saying we will take a hands-off approach and not enforce it. host: what is sliding on the ground? these minimum standards, will be allowed to continue? under the section? guest: this is only for people in the individual market. people who are shopping for plans on their own. these are plans that might lack basic benefits.

2:48 am

whether it is numbers of primary care visits, they might have really high deductibles and cost sharing. while the affordable care act says you cannot pay more than $6,300 a year out of your own pocket, plans on the individual market might come with double that. people are at more financial risk. the affordable care act requires changes to these plans. host: marion, maryland, independent line. caller: thank you for taking my call. everyone seems to be concentrated on the signing up process for obamacare, not the type of care that we will eventually receive. the problems that we are experiencing in our county is that the doctors already are putting signs up in their offices that they will no longer accept medicare patients. i am a medicare person, i am 72.

2:49 am

our doctors are no longer being primary doctors. they no longer can admit you to the hospital. only a doctor employed by a can admit you. the end result, our hospital is going under. we have one hospital in our county. that is our problem here. just about everything you say is backwards. we need to concentrate on the type of care that we will be receiving. i have one question. understand, in the law, legal residents can be covered. that would mean anyone with a green card. i am wondering if you could verify that. they are not saying illegal

2:50 am

immigrants, they are saying legal residents. host: thank you. two good points. guest: the law does allow legal residents to shop on the exchange. that is considered a good thing, they want more people, younger, healthier people. a lot of transplants to this country tend to enroll in these plans. that is a case, legal residents are permitted. people who are undocumented are forbidden from accessing any of the affordable care act benefits. that is a point of contention among some people. they are still able to access emergency rooms if they have a catastrophic illness or injury. in some sense, they are still contributing to the cost of health care. as for your point on medicare, there are huge issues with medicare that go beyond the

2:51 am

affordable care act. that does interconnect with medicare a little bit. the issues in which doctors are accepting medicare, issues of entitlement reform. that is the subject of budget discussion beyond the aca. host: a tweet here, a bigger picture view. still do not understand how this is going to keep costs down. guest: the affordable care act? what we touched on earlier, if more people have insurance, this is a law that is primarily about access to insurance. more people get coverage, the more they are able to see doctors on a regular basis, they do not have to worry about do i go to the doctor or pay the rent. when you get people out of the emergency rooms and into primary care, they are not experiencing these catastrophic illnesses

2:52 am

with as much frequency. it reincentivizes the way care is provided, smaller scale things. host: dan, oregon, kyle cheney with politico. the gop line. caller: good morning. i was curious on the affordable care act. it has a build an argument. they are going to be people who get it for nothing and people are going to have to pay for it. i was curious on the number that are signing up for obamacare

2:53 am

across the country. those are the ones that are going to get the subsidies or get it for free. how does this pay for the fact? my other question, i got this screwed up. host: dan, we will let him go. guest: this is the idea. these people -- the people getting covered now, they are still in the health-care market when they get sick or injured. so the idea is if they have access to a plan, even at no cost to them, they are still seeing doctors in a way that they were not able to earlier. yes, the law does provide no- cost or low-cost coverage for people of low incomes, that is who it is geared at. the idea is to get these people covered so that they are not seeking emergency room care. a lot of younger, healthier people who often go without coverage because they do not want to pay for it, by compelling them to do so with the individual mandate that most people do not like, you are getting younger and healthier

2:54 am

people into the pool to bring down costs for everyone. that is the way they hope to pay for it. host: perspective from "the new york times," a congressional memo piece. the lesson is seen in the failed law on medicare in 1989. host: they go back to 1989 and draw a comparison. opponents clamor for repeal. the law was the catastrophic medical coverage act.

2:55 am

guest: if anyone will take part in that, supporters of the aca. i take that back, you see cyclical issues in entitlement rollouts. for example, medicare part d in 2006. there was a rocky rollout, but today people love medicare part d and the prescription to benefits. that story sounds like the rollout, it was not something people wanted but turn out to be catastrophic for people who were behind it. you can look back at these episodes in history about how previous entitlements played out and defined support for your position in any of them. democrats look at medicare part d in 2006 as the parallel. a rocky rollout, today it is part of the landscape no one would touch.

2:56 am

host: a photo in a new york times piece, 1988. president reagan has grown weary of the catastrophic coverage act. president bush saw advantage and it. angry older voters storming a car carrying a congressman. the history of the catastrophic coverage act is a cautionary tale. sweeping changes to consumers who may not be prepared. guest: that is exactly what the supporters of the law are terrified of. that is because there is evidence out there -- the law can be entrenched, it is not so entrenched that you cannot do something about it.

2:57 am

one of the arguments that the democrats have put forward, this is not going anywhere. it is the law of the land. republicans will never repeal this while obama is in office. that history tells you that laws do not necessarily become the law of the land and remain settled. host: texas, democratic line for kyle cheney of politico. caller: hello, thank you. people need to know that the corporations who are worried about the affordable care act -- they are talking about job loss. it is very sad that a person has to keep a crappy job just because they have health care benefits for an ill relative. now they have choices. this has just happened to my nephew. he was able to move to another job because he is now going to

2:58 am

be able to have health care, even though his wife has a pre- existing condition. secondly, we have a wonderful system in this country. the problem has been access. i think that needs to be emphasized. access is the problem. emergency room care is the most expensive care in the world. the republicans put up a plan, i think it was romney, it covered 5 million people. i mean, they are the ones that won vouchers for medicare and so forth. lastly, if people do not want to sign up for the affordable care act, they should keep whatever crappy care they have. who do you think they will blame when they get sick?

2:59 am

guest: job lock, the first point you made, something i have heard and to make this point a bunch to support -- i have heard nancy pelosi make this point. if you leave a job, you are no longer tethered to a bad job. you can start your own business without the risk of not having insurance. there is a potential transformative element there. one that the proponents like to talk about. you also mentioned the point on access, which is true. emergency room care is extremely expensive. axis is not the only issue. one of the problems they saw in massachusetts, which past and access law in 2006 under romney, you could get everyone in the state insured and still have soaring costs.

3:00 am

they have passed subsequent legislation to tackle this. it is not a panacea just to get everyone covered, it may have some benefits. host: twitter, "end of life treatment is the primary driver of costs?" life witter, "end of treatment is the primary driver of costs?" guest: end of life treatment gave birth to the political andment over death panels issues about dealing with people as they dash at the end of their lives. one of the things that people in the medical world say there is not enough of that kind of -- hospice care, pellet of care -- -- care thatre helps people cope with death.

3:01 am

in some sense, that is a solution to costs. not in the way that people who worry about death panels described, but there is an option for people to do it in a more controlled way towards the end of their lives with input from doctors that they are not accessing now. host: another tweet. "what is the affluent person wants to buy more insurance than the single-payer?" guest: there is the cadillac tax, the tax on cadillac plans that are really generous. that is to get out the overly generous plans thapeople are enjoying themselves for people that whenever used. host: arlene, florida, democrat. good morning. caller: thank you for taking my

3:02 am

call. i want to address, when mr. obama said if you like your plan you can keep it. in my opinion, he lived up to that. the reason i say that is because , as we know, when the law was 2010,ed -- implemented in the old plans were grandfathered in. at what point do insurers have the obligation to tell 2014, these plans will be obsolete. show them other options. i hear a lot of blaming president obama. i do not hear a lot of culpability being placed on the shoulders of the insurers themselves. at what point will we start hearing these insurers being held accountable? canedy administration -- the administration do better in

3:03 am

presenting exactly what these plans contain and what they really are worth, basically nothing. thank you. if you could elaborate on that. guest: thank you. the president got into trouble over his semantics. your point is one thing that they try to make as this issue became more combustible in rece nt weeks. the president always knew that insurance companies could pull the rug out from under you. his point was they do not have to, they can grandfather you in. his issue comes because people knew at the time that although they could grandfather you in, a lot of them would not do that. to say it unequivocally has gotten him into political trouble. he has apologized. in that sense, that is where the comesomes from -- furor from. i don't think insurers will take

3:04 am

the plan -- the blame for that. one pl -- when plans reoffer these canceled policies, they have to also let the plans observers know what they do not cover, what benefits are omitted from that that would be there if they sign up for an affordable care act plan. that puts the insurers on the spot, you can have your old plan, we will not cover you in x, y, and z situations. you might be better off in the marketplace. host: thomas, san diego. of the market, individual plans, causing the chaos. most of us get our insurance through employers. the last couple years, my contribution to my employer plan has gone up considerably. i am promised by my cfo that is

3:05 am

going to go up next year. how much is this going to cost us, what effects this is going to have 180% of us start getting premiums go -- when 80% start getting premiums going up? i wonder if that was why it was postponed. is anyone looking into that affect? point point.aise an interesting the employer mandate was geared at a small subset of large employers. employers with more than 50 employees who do not provide coverage at all to workers. the affordable care act says you have to come in with compliance with the health care law, one of those requirements is if you are a large company, you have to provide coverage to your full- time workers. aboutis a lot of issues how that works. the delay of a yet raised -- a y ear caused outrage among

3:06 am

opponents who said you are going to exempt employers, why are you exempt people who also have to get coverage. you are really talking about a small subset of large companies that do not already provide coverage. as for the cost of coverage that large company provide, that is an issue. that is separate from the meeting itself -- from the mandate itself. as for large companies that offer insurance, it is the vast majority. we are talking about a small subset that are enjoying the benefits of the delay that mandate. host: bill, kentucky, republican. whyer: i would like to know the democrats and obama are standing up and lying about this, saying it is going to be cheaper for anybody. if you had a pre-existing condition -- nobody is talking about -- talking about pre-

3:07 am

existing conditions. my son's insurance went up 20% because of that. sick, he willets have to pay $300 a month, he can get it now for $80 a month. the younger people and the seniors are going to be hurt by this. -- the democrats claim that the us having to buy insurance, the mandate, this is going to affect anybody under $100,000 except about 15 million who are going to get it for free. the rest of them are going to be $200 to $600 a month. when it started, i said that there would be 31 million not insured, the cbo has backed that

3:08 am

up. about 14 million or 50 million will be insured. i would like to know why nobody is speaking to this. nobody is telling the cost of these people under $100,000, up to $100,000, they keep talking about the subsidy. host: bill from kentucky. onst: the point you touched at the end, there may be part of the cost of the overall law, the subsidy is designed for facing people who are facing premiums that are unaffordable. if you can provide a plan in your marketplace that costs less income, you are required to buy it. if your income is such that -- you are below 400% of the poverty level, which is about

3:09 am

$11,000 for an individual, you will get help. that could be if you are just over medicaid, you may get a portion of your premium covered. if you are under that, you will get on medicaid. you talked about people under $26,000, those are younger, healthier people. those are the people they are trying to get insured to bring costs down. host: a tweet. john in north carolina. how long does it take before policies are canceled? guest: i don't know the exact amount of time, it is an interesting point. one of the nuances in the numbers the initiation released released,tration the people enrolled have not necessarily pay their first months premium. that is how the insurance industry measures enrollment. you have to pay your enrollment before you are enrolled.

3:10 am

one of the metrics we will have to watch going forward is how many people pay their first months premium. and how many make recurring payments. that shows that they are able to afford it. host: kyle cheney, health-care reporter for politico. a native new yorker who went to ran theniversity and campus newspaper. he moved onto the scene house ate house news st service in boston. what percentage of politico's resources are spent on the story? guest: it is huge. i have been at politico 1.5 years. even during the election last year, the intensity around the coverage, in washington, i have not seen anything like it. it is fascinating to be a part of and to cover. it does not show any signs of

3:11 am

abating. host: how to get get up to speed on something so complex? guest: once you think you understand everything, you get a new wrinkle. it is a constant learning process. the question i get is have you read the whole thousand page law. the answer is probably not from beginning to end, but at some point or another, you have gone through every provision. host: take us back to the hill. with thesecurity affordable health care act. we have seen hearings about it. where is that issue right now, where is it headed? guest: computer security has been an issue, primarily because the roman system is broken. republicans, not just republicans, people have found sets of vulnerabilities indian roman site -- in the enrollment

3:12 am

site. if people are entering an permission cannot be compromised by a hacker? i learned that the agencies overseeing this employer on -- hackersheir own ethical to patch these. it is a subject of intense scrutiny and oversight, especially from people who have questions about the law as a whole. there has been tremendous assurances from the administration that these exchanges are airtight. if not, they are doing everything to make them airtight. that is part of the november 30 fix. partdicated to security as of the triage team of repairing healthcare.gov. other kind of hearings are you expecting? aret: no end to hearings we going to see. part of this is a political

3:13 am

statement. the republicans have said they ,ant to use oversight as a tool to put a microsoft to the health-care law. a arthroscopeut -- a microscope to the health- care law. in addition to what we have seen with kathleen sebelius and marilyn tavenner, they may want againr from the top brass as to whether they want to update their thinking on a law. we may get more big picture stuff in december. host: more about life on the hill. here is "the wall street journal." thatg the point immigration, tax reform, a budget breakthrough, things are on hold or frozen. what does it mean? guest: the affordable care act

3:14 am

takes oxygen out of the room. it is so politically potent. it affects everyone's constituents. they are getting the most calls on it, too. it provokes strong feelings. the agenda has come to a standstill, there is evidence that some of these things were at a standstill already. the affordable care act, that is how you fill the vacuum at a standstill. over the summer, when immigration was a big topic. when it became clear that that was stalling, the affordable care act came back with a vengeance. that was the issue everyone wanted to talk about. there is some truth that it gets in the way of everything else. also, it is a fallback for people when they cannot talk about other things. marion,t's hear from kentucky, thank you for waiting. you are on with kyle cheney of politico. democratic line. caller: good morning. my family doctor,

3:15 am

our family's dr. of 34 years has the affordable health care. he told us that is why he was quitting. town on therural ohio river. there is not a doctor on -- i am 66 years old. there is not a doctor that will take a new medicare patient in a 50 mile radius. they do not take new medicaid patients. i understand most of kentucky's enrolees are medicaid. what good is our insurance if we don't have a doctor? explain to me, thank you. fear, it is a real especially in rural communities, that access to health care, it has already been a problem. let alone the impact of the affordable care act, that does

3:16 am

not necessarily hurt access to care, there is a sense that it does not do enough to help. a lot of these communities have one, maybe two health-care providers that they rely on. we learned in new hampshire recently, there is only one insurer offering a plan on the exchange. that is sure that insurer decided that only 16 oof the 26 would offer care. is a huge issue. not to mention the supply of doctors. there is a crisis of the number of doctors in this country before the affordable care act. when you add millions of people, that only adds strain on the number of providers. that is an active problem that has heightened in a rural community. it is a nationwide issue. host: why is there a shortage of

3:17 am

doctors? guest: i don't know the root cause. it takes a while for demand to catch up -- for supply to catch up to demand. it takes so many years to train a doctor. once the affordable care act past, it has been three years. medical world, that is not full training. along the atlantic --- there is a long pipeline. you may not have enough to capture the full newly enrolled population. host: deal, florida, independent caller. caller: good morning, thank you for taking my call. a couple quick points. of thebout the legality health-care law. the judicial branch said his legal. -- it is legal.

3:18 am

what is the next step? can we force people to buy car insurance, even people without drivers licenses. can we force renters to buy homeowners insurance. one day they may need this. that is my question. it was a lot longer. i am trying to cut it down. guest: that is the slippery slope argument that opponents made in court and outside of court. the administration argued specifically that the health care market is unique. ,veryone is in it at all times you may not realize it, but if you get injured, the hospital is required to take care of you. that does not hold water with justices who did not find merit and not. -- in that. it was part of the argument. it would be hard for them to come back and say we also meant that for car insurance, too.

3:19 am

or home insurance or whatever. it would be hard host: we will spend 10 minutes with our guest. he will answer a lot of questions. he has been with us the whole hour so far. fort lauderdale in florida -- republican. caller: good morning. i would like to say that i am a veteran. i fought in the war for freedom of choice. i did not think that we were going to be like communistic russia. dictate that you cannot have freedom of religion, freedom of choice, and what ever you choose to do health care wise. i would like to ask why are we being forced to have health care insurance by the government

3:20 am

mandate? guest: this touches on the point i mentioned earlier. the idea promoted by supporters of the flaw is that everybody needs health care at some point in their lives. there is no escaping it. accessyone is going to it and be part of the cost of health care, then we should take the measured step of getting covered. fromll prevent them wasting their cost on the rest of society. that was it in a nutshell. republicans used this argument in support of the mandate of the past. governor romney supported that point. the narrative flips and now it is democrats making the argument. a lot of people still find that it does not carry weight. at the end of the day, it compels people. some people may not have ever wanted to purchase insurance and now they do so.

3:21 am

you may never be able to get on board with that. the idea was that, for the benefit of society, you compel a small subset of people to purchase something. host: mary -- good morning. caller: i wanted to straighten out something. i was under the assumption that once the affordable care act , it was kathleen sebelius that made the regulations change for insurance companies. could you just straighten this out? guest: absolutely. if you read the whole lot cover to cover, you would not know the significant part of how about laws applied. so much was written in regulation. kathleen sebelius did have to sign off on regulations in terms of benefits that are offered. what is acceptable cost sharing? much of this law is in

3:22 am

regulation. republicans made a twitter mountain of paper that symbolizes all of the regulations that have been passed. it is hefty. host: you can watch her testimony and all of the hearings that we have covered on our website, c-span.org. the video library is there. go to it and pick. mike is calling from maryland. democrat. good morning. caller: my question is concerning the access issues related to her -- provider participation. pharmacies,spitals, -- i am hearing people say that they cannot get doctors in their area. they have to leave the doctor that they had. they have to go further to hospitals that made it before.

3:23 am

i am also wondering if the insurance may be continuing to models -- ppo models. guest: that is a good point. one of the things we're seeing a lot of and the exchanges is that the plans are keeping their costs down by narrowing down networks. they are saying that you can sign up for a plan, but you can only go to these specific hospitals. that is the hmo model that you talked about. it is something that, if people are cost conscious, they might value. if they value choice more than paying a higher premium, they may be very frustrated. their local hospital may not be in the network. suddenly they are driving a good distance away to get the care they normally would have gotten around the corner. this will be a story of the upcoming year.

3:24 am

we will see this take effect and people will start to either appreciate them because of the cost value or become frustrated because they cannot go to their local facility. host: take us back if you could. following the president's action on thursday, the house vote on the bill on friday -- remind us of what is in the senate. who has put out what ideas? --st: senator landrieu has she is a democrat from louisiana who is up for reelection. she sponsored a bill that is upton light. it would have the effect of giving the ability to remain on substandard plans that do not meet the aca standards. it is thornier for democrats .ecause they may be vulnerable they capture the sentiments of

3:25 am

people in their district. if they are not reelected, it could threaten the majority for senator reid. what they will allow -- i am not 100% sure. than need to go further what the president has suggested, we well. it seems to me to leave the door open. this goes beyond what the president says and gives democrats a chance to say that they voted to protect the plan. host: you can watch live coverage of the senate on c- span2. they have nominations in defense spending and some other items for people to talk about. jose,is calling from san california. republican. good morning. caller: thank you for taking my call. i have been listening to the experts on tv and the experts on talk radio talk about all things

3:26 am

involving obamacare. there are 90 trillion dollars of unfunded liability coming down the tracks. we do not have money for this. passed,this thing was we will find out what is in it. some will live, some will die. i am really concerned that it will be -- i at thousand -- death by 1000 flashes for a lot of people. will decide what operations you get and what kind of drugs you get. one way to solve this liability is to call the population -- cull the population. you do not pay benefits for people who are dead. guest: your first point was on entitlements and the huge

3:27 am

massive unfunded liability that the nation is facing. both sides of the aisle acknowledge this. it is another venue of the budget committee. there are members of the senate and lawmakers who are looking at how to tackle long-term funding issues for things like medicare, medicaid, and social security. they go far beyond the affordable care act. this is something that will come to a head in the next month and in january, when we reach the deadlines. hopes thatf high they will come to a grand solution. i think that is definitely on the docket. host: one last call. burrell from maryland. independent. caller: good morning. i am for freedom of choice also. my question to you is -- i see

3:28 am

so many doctors. i want to stand behind the aca. as a black man, is there anything in the law that allows us to find doctors from outside of the system? cuba or some place? they will work for less money. is there anything in the law that will prevent us if we want to go outside of this community to find doctors? sure that thet law speaks specifically to allowing someone to look outside of the country to find care. i do not think it would prevent that either. is pretty focused on domestic health care access. host: what is next for you? guest: that is a good question. we will see how the president promised plays out over the next few weeks. state take them up on the

3:29 am

offer? it seems like they are not. -- january 1 is when people start get coverage. or lose coverage if they have not found an alternative. that is a significant date in the timeline. we will write about that in the run-up area host: you can read his work at politico.com hospits

3:33 am

away. and he asked how can the best health care in the world cost twice as much as the best health care in the world? same question has occurred to a lot of smart people involved in paying for health care in the private sector, and they came up with reference pricing as a partial response. and we've assembled several of those smart folks today on our panel to explain how this mechanism works, what the challenges are in putting it in place and whether plans like medicare and medicaid could draw lessons from this experience. now, we're pleased to have today as our partner wellpoint

3:34 am

incorporated operator of the blue cross blue shield plan in more than a dozen states which collectively cover about one in nine americans. and you're going to be hearing there michael bell monday from wellpoint's anthem health plan in a few minutes. let me take a couple moments to cover song logistics -- some logistics. there is a lot of biographical information about our speakers in your packets. you'll also find in hard copy the powerpoint presentations of our speakers. those slides and all of the background material those of you in the room have in your kit are available on the alliance web site, www.allhealth.org. also on our web site you can i view a webcast of the briefing in a couple of days and a few days after that, a transcript of today's discussion. now, of course, if you're watching on c-span, you have the

3:35 am

video. you also have access to all of the materials i mentioned if you have a computer as well and go on to our web site, allhealth.org, and you can follow along with the slides, among other things. i would ask you at the appropriate time to fill out a blue evaluation form to help us improve these programs as we go along, make suggestions about speakers and topics that you'd like to hear from and about, and this is also a green question card. when we get to the q&a, there are both microphones you can go to to ask your question or to write it on the green card and pass it forward. if you're part of the twitter verse, you can make use of the hash tag @reference pricing as you see up on the slide that's in view now. and that's enough of the preliminaries. we have, i believe, just a

3:36 am

marvelous assemblage of folks with knowledge and insight into today's topic. you'll hear their presentations, and then we'll get into the discussion and the q&a. and we're going to start with andrea who's the program director at catalyst for payment reform. and if you're not familiar with cpr, as it's appropriately abbreviated, it's a nonprofit working with large employers and other purchasers to improve how we pay for health services and to promote high value care. andrea's had a decade and a half's experience inning with a focus on benefits and payment policy, and we've asked her to provide an overview of reference pricing today; how it works and what some of the challenges are. andrea, thank you for being with us. >> thank you, ed. thanks to the alliance and for wellpoint for convening this

3:37 am

really important meeting. i think you'll hear some really great case studies from the folks on the panel, and i'll be giving a background and, actually, ed gave of actually a pretty good definition for -- on it. and i think cpr is catalyst for payment reform, as ed mentioned, is a nonprofit national organization that works on behalf of national large purchasers. we have about 31 purchase efforts that -- purchasers that work with our group, and they include eight state agencies. and of those state agencies, we do have four medicaid plans. so to the previous point about can state agencies and medicaid programs learn there some of this, i would say that in the work we're already doing, there's a lot of shared learning that's occurring. one thing that the cpr members agree to do when they join is to work on a shared agenda, and i'm not going to get into all of the

3:38 am

details of our shared agenda, but the middle section there on the right-hand side will talk about our innovation, so i'm going to touch on three of those today. the first, obviously, is reference pricing and value pricing. the second is price transparency, and the third is market power. and all three of those items are really closely related. and you can't really talk about reference pricing without also talking about market power and the need for price and quality transparency. at its core, cpr has -- our strategies fall into two categories. and it sounds simple, but it actually can be kind of complicated. but basically, we're trying to create a critical mass of purchasers to send the same messages into the marketplace at the same time. and that's how we think we'll really change the market. we've got a lot of noise, a lot of people asking for different benefits, different payment, different ways of doing things, and that can really exacerbate confusion. so the cpr purchasers are trying

3:39 am

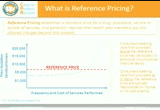

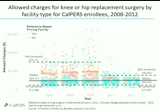

to use common tools, common language, common priorities to send messages into the marketplace about what's important. and, of course, the second is to shine the light on the urgency for payment reform as our name is catalyst for payment reform, after all. so this might be a little difficult for you to see in the orange text, but if you look at your printed version, it might be a little easier. as ed mentioned, reference pricing really is just setting a standard price for a drug, a procedure, a service. and then once you've set that price, that's the amount, the allowed amount that the health plan or self-insured employer pay. and above that amount the consumer is likely to have additional out-of-pocket financial liability. if you look at the graph there, on the y axis you see price variation. this is really just for illustration purposes. you'll see different variation in prices ranging from a

3:40 am

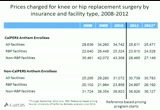

thousand dollars up to $20,000. and then along the bottom you see the frequency of these services. and the blue line kind of shows how often are these procedures taking place and at what price and then where do they go up. and this is the kind of analysis that has to take place. so you can set a reference price, but it's actually quite complicated in doing that. a lot of analysis has to go into doing that. i'll give you an example other than calpers or kroger, but safeway did analysis of how much they were paying for colonoscopies in the san francisco bay area, and the prices ranged from $900 to $7,200 with no correlation to quality. so that's an extreme variation in price. and once they did the analysis on the price and they saw the frequency of how many visits were at a certain price or below, they pegged their reference price at $1,250. so then their benefit design, as

3:41 am

they implemented it, if you are a consumer, safeway employee and you seek care can from a provider that is at or below the reference price, $1,250, then you either have no cost sharing or no -- or your regular cost sharing. if you seek a provider at that $7,500, at the top of the list, then you are going to be responsible for the difference between the $1,250 and the $7,200. so that's the mechanism of how reference pricing works. and some actually will consider it to be a pretty blunt instrument in the marketplace, and i think you'll hear how it's a blunt instrument, that it really is intended to shake up the marketplace and really shine the light on not only how things are being paid for, but what are the prices for things and how there's just extreme variation without any correlation to quality. i'm sure you'll hear from my colleagues that there are really four key elements of reference

3:42 am

pricing. they'll probably go into more detail about these different elements, but basically there's benefit design. you really only want to implement reference pricing when it's elective and when you have a wide availability of providers. obviously to, this isn't going to work if you have one or two providers providing a service in an area. that is not going to create the level of competition that you need. so, one, the procedures have to be elective, and there's time to shop and, two, they're available for multiple providers. the next two are really interrelated and, i think, are very on topic for conversations in this room which is price and quality transparency. you can't implement a reference price without giving consumers adequate information about the price of the procedure or the quality that they're receiving. most consumers still equate higher price with higher quality, and we know that not to

3:43 am

be true. so you really need to arm consumers with plenty of price information so they know which providers are at or below the reference price, and you also need to arm them with the quality information, how often are these providers performing these procedures? what is their volume? what is their outcome? and if you have that information, then you can -- consumers are better armed. but it would be with really unfair to implement a reference price if you aren't going to arm them with that kind of information. that goes into the next one which is consumer education, and i think there will be case study examples of how informing your employee population and educating consumers about the price and the quality and that the -- and the correlation between the two will be really very important. because you don't want consumers to get into a gotcha situation where they didn't know someone was above the reference price, and now they have a pretty extreme financial out-of-pocket

3:44 am

liability. and the last one is add yacht networks, and network might not be an appropriate term here because usually these are providers within an already established network, so i use the term "network" loosely. but you want to be able to make sure that you have plenty of providers who can offer these services, these procedures at the reference price so consumers have the ability to choose, and they don't feel overly limited. they have plenty of options including the option to go to seek the care from the provider over their reference price, but that's their choice. i won't go through all the detail, but this is a schematic of reference pricing. you have very basic all the way to really more mature and sophisticated. and cpr also likes to talk about value pricing. reference pricing really refers to commodity-type services like

3:45 am

lab, imaging. and value pricing -- or, excuse me, commodities services, that's really where for services where quality is thought not to vary. when you move into value pricing, you're actually adding a quality component and quality can vary. so as you get to the higher end of that spectrum, that's when quality gets inserted. and again, when you look at the safeway -- when they applied reference pricing to their colonoscopies and they've now applies it to other procedures, they were able to hold their per capita health care spending flat. and i think you'll hear from calpers about the savings that they were able to achieve. and i think as we go into, you know, what's next for reference pricing, you'll find that reference pricing is going to gain in popularity. only about 5% deployed this strategy in 2013, but we expect closer to 15% in 2014. that's from our recent towers

3:46 am

watson/nbgh study. i want to go back to this issue of price variation because one of the things reference price does, why implement reference pricing, one of the main reasons you do it is to really bring a huge spotlight on the price variation and how it is unwarranted. and market power will drive the price, and price is the leading cause of health care growth today s. so reference pricing is a way for employers, purchasers, those that we work with to really say that that price variation is no longer tolerable. what's next for reference pricing, um, a couple of things. price transparency and quality transparency. ..

3:47 am

>> and it's actually a natural fit, bundled pricing -- excuse me, bundled payment is a packaged price for lost procedures within a particular service, let's take a hit or a knee replacement. easy multiple providers in multiple settings. a bundled payment is for all of that. then if you set a reference price, you really are making it very clear what's included in the reference price. the providers are clear about what's in the bundled payment and we see that road as the next generation, once we get a little more experience with pure reference pricing and the providers get more experienced

3:48 am

taking bundled payment i think we will see a hearing of bundled payment and reference pricing. so with that i guess i will turn it back to you, ed. >> thanks very much, andrea. we are indeed next going to from david cowling who's the chief of the center for innovation at calpers, california public employees' retirement system. you may know that calpers is a lot more, you might imagine from the title of its organization it administers health and retirement benefits for more than 3000 public schools and agencies and state employers, and covering more than -- 1.3 million health plans to david is here to tell us about calpers reference pricing program and its impact on health care and costs, as andrea said that he might, and promised that he might. thank you for coming.

3:49 am

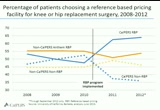

>> thanks, ed. i'm going to talk about calpers -- hold on. i'm going to talk about calpers state pricing program for hip and knee replacement. as ed alluded to, calpers provides health benefits for about 1.4 million members statewide. that includes active and retired state employees, and about 1200 local agencies including school districts. about a third of those end up in the preferred provider organizations with anthem blue cross of california and we spend about 7.5 billion annually and health benefits and i don't know about in washington but in sacramento that's a little bit of money. so the impetus for state pricing with a variety of studies and they all have different purposes, but they ended up kind of helping guide reference-based

3:50 am